The Gallery of Crowd Behavior Returns May 2, 2011

Doug Wakefield

“

[From an intensive two-year study], I found that market price movements are

like people – they have statistically significant life expectancy profiles that

can be used to measure risk exposure…Consider life insurance, which deals with

the life expectancy of people instead of price moves. If you’re writing life

insurance policies, it’s going to make a great deal of difference whether the

applicant is twenty years old or eighty years old…. Similarly, in a market that

is in a stage of old age; it is particularly important to be attuned to

symptoms of a potential end to the current trend. To use the life insurance

analogy, most people who become involved in the stock market don’t know the

difference between a twenty-year old and an eighty-year-old.”

Hedge

Fund trader Victor Sperandeo in The New Market Wizards: Conversations With

America’s Top Traders (1992) Jack Schwager, p 256

On

November 2, 2007, I released a short article titled A Gallery of Crowd

Behavior. The objective was simple. Display a set of charts across a variety of

markets, in an attempt to point out that major turns in markets, when they

come, are not a total surprise to those who are looking for them, and charts

are the picture that are worth more than a thousand words at key historical

points. It is my belief, that the odds are extremely high, that May 2011, like

January 2000 and October 2007, should be one of those times. Since my opinion is of no value in and of

itself in the sea of human opinions, I only ask that you examine these charts,

and consider their relation to previous tops, and the concept of age as

explained by Mr. Sperandeo in the opening quote.

Three Tops

Last

Thursday, I decided to study the previous tops, and compare them to the Dow’s

jet propulsion movements since its March 16th at 11,555. What I

found was quite interesting.

If

one looks at the trading days leading up to the January 14, 2000 top, they can

see a bottom 31 days prior to that top. We can see a bottom 31 days prior to

the October 11, 2007 top. And, if we

start at the bottom on March 16th, on can see that Friday, April 29th,

marks 31 days from that trading bottom.

The

last 31 days leading up to the January 14, 2000 top pushed the Dow up 891

points. The last 31 days to the October 11, 2007 top pushed the Dow up 1164. In

the 31 days of trading between March 16 and April 29th, the Dow has

moved up faster than both of these previous tops, leaping 1277 points.

Now

one mighty say, “Yes, but Monday, May 2nd, the Dow moved even

higher”. While this is most certainly correct, why would someone ignore the

parallels between the 2000 and 2007 top, especially if the speed of ascent

today (AFTER the fastest bull market in US history) was even faster. Shouldn’t

any investor or trader perceive our current juncture with extreme caution,

rather than EXPECTING a very old trend to continue climbing into the

stratosphere?

Two Aircraft Carriers

Anyone

seeking to understand developments and data in the global currency and

derivatives market would read the Triennial

Central Bank Survey on Foreign Exchange and Derivatives Market Activity

(April 2010). The most recent survey was released in September 2010. The

following helps us understand the enormous size of the global currency market,

the largest market in the world:

“Global foreign exchange market turnover was 20% higher in April 2010 than in April 2007, with average daily turnover of $4.0 trillion compared to $3.3 trillion. The increase was driven by the 48% growth in turnover of spot transactions, which represent 37% of foreign exchange market turnover. Spot turnover rose to $1.5 trillion in April 2010 from $1.0 trillion in April 2007.”

I don’t know about you, but the numbers in the BIS report are almost incomprehensible. While the currency markets are experiencing a turnover of $4 trillion a DAY, the April 2011 release on the World Development Indicators by the World Bank, reveals a global GDP of $59 trillion (Atlas method), and the US GDP of $14.1 trillion ANNUALLY, and the US deficit stands at $829 billion ($0.8 trillion) at the midpoint in its fiscal year.

Let’s compare these three massive numbers once again.

· Annual turnover in global foreign exchange market – (assumes 260 trading days) - $1,040 trillion.

· Global GDP - $59 trillion; U.S. GDP - $14.1 trillion

· U.S. Deficit, largest in its history – on pace for $1.6 trillion.

When one looks at these numbers, it is like talking about the distance to the nearest star or the speed of light.

The next chart makes it very clear, that the largest currency trade in the Forex market is the US/Euro trade.

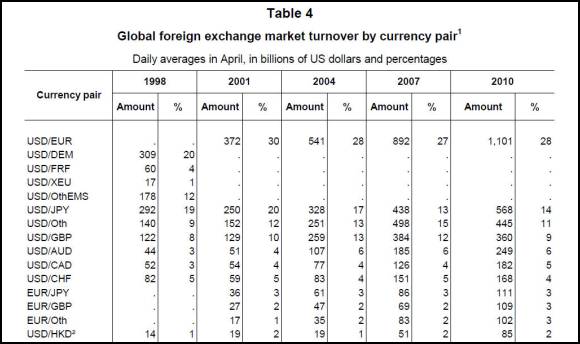

[BIS Triennial Survey: FX and Derivatives Activity in Apr10, rel. Sep10 – pg 10]

Based on this information, it would seem extremely important for anyone depending on our global capital markets to pay attention to trends in the US dollar and Euro. From looking the charts below, and once again considering the comments of Mr. Sperandeo earlier, it would appear that a massive change in direction should be expected for these two aircraft carriers.

With the Euro sporting one of its highest bullish sentiment readings since its bottom in June 2010, and the US dollar providing one of is lowest bullish sentiment readings from the same period, it would seem to behoove us to think as contrarians, and look for the end of these trends and the start of new ones. This is not an argument for the long-term sustainability of either of these currencies, as they exist today, only a reminder that trends change along the way in this historical journey.

When one compares the patterns in US equities since last June, with that of the US dollar, it seems to beg the question, “Could these two powerful markets change trends together?; How could these changes impact other capital markets?”

These words, written by Nassim Nicholas Taleb and Mark Blyth in the May/June Issue of Foreign Affairs, should make us all think hard about the current level of risks in global markets:

“Complex Systems that have artificially suppressed

volatility tend to become extremely fragile, while at the same time exhibiting

no visible risks. In fact, they tend to be too calm and exhibit minimal

variability as silent risks and accumulate beneath the surface. Although the

stated intention of political leaders and economic policymakers is to stabilize

the system by inhibiting fluctuations, the result tends to be the opposite.”

As

I continue to remind my subscribers, expect the unexpected.

If you are interested in our

most comprehensive research and trading commentary, consider a subscription to The Investor's Mind:

Anticipating Trends through the Lens of History.

Doug Wakefield

President

HUBest Minds Inc.UH, a Registered Investment Advisor

2548 Lillian Miller

Parkway

Suite 110

Denton, Texas 76210

Phone - (940) 591 - 3000

Alt - (800) 488 - 2084

Fax - (940) 591 –3006

Best Minds, Inc is a registered investment

advisor that looks to the best minds in the world of finance and economics to

seek a direction for our clients. To be a true advocate to our clients, we have

found it necessary to go well beyond the norms in financial planning today. We

are avid readers. In our study of the markets, we research general history,

financial and economic history, fundamental and technical analysis, and mass

and individual psychology.

Disclaimer:

Nothing in this communiqué should be construed as advice to buy, sell, hold, or

sell short. The safest action is to constantly increase one's knowledge of the

money game. To accept the conventional wisdom about the world of money, without

a thorough examination of how that "wisdom" has stood over time, is

to take unnecessary risk. Best Minds, Inc. seeks advice from a wide variety of

individuals, and at any time may or may not agree with those individual's

advice. Challenging one's thinking is the only way to come to firm conclusions.

Copyright © 2011 Best Minds Inc.