A History of Unlimited Money:

Learn From It or Repeat Its Mistakes, August 28, 2014

Doug

Wakefield

Thursday,

August 28, 2014. Is there anything special about this day? For some it may be

an anniversary, marriage or work. For others it may be a birthday. However,

chances are it is just another day of the week, following the same routine as

last week for hundreds of millions of lives that depend on an economic and

financial system they hope will stay predictable.

For Americans today, the answer that has been presented to us

repeatedly for years, and sadly seems to have been accepted as necessary to

restore our capitalist system, is that the Federal Reserve will merely print up

trillions more in debt in order to bring things back to “normal”. History is

replete with lessons for the Federal Reserve, Keynesian economists, and

millions desperate to believe that maybe this time, with trillions more in

debt, the temporary riches of the financial markets will become permanent and

predictable. Frankly, the only thing predictable about this story is that

history keeps repeating itself, and we do not show any desire to learn from our

past.

For Americans today, the answer that has been presented to us

repeatedly for years, and sadly seems to have been accepted as necessary to

restore our capitalist system, is that the Federal Reserve will merely print up

trillions more in debt in order to bring things back to “normal”. History is

replete with lessons for the Federal Reserve, Keynesian economists, and

millions desperate to believe that maybe this time, with trillions more in

debt, the temporary riches of the financial markets will become permanent and

predictable. Frankly, the only thing predictable about this story is that

history keeps repeating itself, and we do not show any desire to learn from our

past.

In order that we are all clear that history is a great resource to

avoid mistakes we continue to ignore today, we will start with two events in

the 1700s that demonstrate why the “Icarus can print money to reach the

stability sun” theory has already failed miserably. Remember, these stories are

centuries old.

In order that we are all clear that history is a great resource to

avoid mistakes we continue to ignore today, we will start with two events in

the 1700s that demonstrate why the “Icarus can print money to reach the

stability sun” theory has already failed miserably. Remember, these stories are

centuries old.

John Law and the Mississippi Scheme

John Law and the Mississippi Scheme are

well documented for anyone interested in the history of finance. For that

reason, I will focus only on a few points in this short synopsis. I encourage

you to think about how this story relates to the world we have lived through

merely since the start of the 21st century.

For

years the investment mantra “Don’t bet against the Fed”, has been viewed as the

elixir to almost unlimited riches for investors and money managers. And yet,

twice in the last 15 years we have lived through the two most destructive

deflationary periods in asset values in the history of finance. Even now, we have seen in the last 2 years

the major central banks welcome ever-poorer quality collateral to back loans to

speculators, (1) all in an ongoing effort to continue inflating

global financial bubbles to even greater extremes in price and behavior.

None

of us today can conceive of a world where currencies were backed by gold. And

yet, the practical benefit of this was seen about a century before the

Mississippi Scheme entered the history books.

In 1609, the Dutch set up the first

central bank in the world, the Amsterdam Wisselbank. The bank kept bankers and

investors separate, which proved crucial in 1637 when the Dutch Tulip Bulb

mania collapsed. The bank paid no interest on deposits, and made no loans. It

practiced 100 percent reserve banking, and notes were issued only against gold

holdings. (2) Since the financial sector was separated from the

banking and government areas, the damage from the wild speculation on tulip

bulb prices impacted individual investors and the financial sector, but

preserved the banking and government sector for the nation. In other words,

there was no need for the citizens of Holland to be informed of an urgent need

for a bailout of their banks or speculators. Oh that’s right, we call ourselves

“investors” today.

In

1694, the same year that the Bank of England was formed, a man named John Law

fatally wounded a man in a duel, was convicted and sentenced to death, and fled

to Europe to spend the next 20 years as a professional gambler. Sounds like an

excellent person to have as the lead advisor to the King of France, don’t you

think? (3)

Law’s

ideas went into practice, when he responded to a public plea from Philip II for

an astute financier who could save France from bankruptcy. It wasn’t long  before Law’s ideas were put into practice in 1716, when the Banque

Generale was founded. Philip II’s uncle, the Duc d’Orleans, had been placed in

charge of the royal finances, and the Duc declared that all taxes must

henceforth be paid with notes issued by Law’s bank. This was the first time in

modern history that a government sanctioned paper money. (4) (5)

before Law’s ideas were put into practice in 1716, when the Banque

Generale was founded. Philip II’s uncle, the Duc d’Orleans, had been placed in

charge of the royal finances, and the Duc declared that all taxes must

henceforth be paid with notes issued by Law’s bank. This was the first time in

modern history that a government sanctioned paper money. (4) (5)

Unlike

today’s holders of paper currencies, Law declared that his notes were

redeemable at site for the full amount in coins. This idea became the prototype

of the gold standard used by the British, French, and the majority of European

currencies through the 19th century.

The

final phase of Law’s plan, in theory, involved the backing of his paper money

by land. Instead, Law convinced Philip II to back a trading company with monopoly

trading rights over the Mississippi River and France’s claims to land in

Louisiana. Shares of the new company were offered to the public. His monopoly

allowed him to also mint royal coins for 9 years as well as act as the royal

tax collector.

As

time went on, the people started using the newfound money, and as it changed

hands, trading and commerce flourished. As the scheme continued to work, the

Duc renamed the bank, the Banque Royale, and by 1719, it had issued 1,000

million new banknotes, increasing the money supply 16 times the previous

amount. (6) Hmm, rapidly increasing the money supply to make people

feel richer? Now where have I heard that before?

As

you read this quote from Charles MacKay’s well known work, Extraordinary

Popular Delusions & the Madness of Crowds, remember that this book

was first published in 1841:

“The public enthusiasm, which had been so long rising, could not resist a vision so splendid. At least three hundred thousand applications were made for the fifty thousands new shares, and Law’s house in the Rue de Quincampoix was beset from morning to night by the eager applicants…Dukes, marquise, counts with their duchesses, marchionesses, and countesses, waited in the streets for hours every day before Mr. Law’s door to know the result….they took apartments in the adjoining houses, that they might be continually near the temple whence the new Plutus was diffusing wealth.”(7)

The “apartments” “near the temple” have been replaced by one’s speed

of light computers next to the exchanges, which work off a strategy of starting

and ending each day owning nothing, meanwhile leaving today’s counts and

countesses still believing they live in a financial world lead by long term

investors. Only when the busts phase sets in with earnest, will they begin to

wake up to learn that 2% of the 20,000 or so trading firms that made up 73% of

all U.S. equity trading volume have left them holding the bag. (8) (9)

The “apartments” “near the temple” have been replaced by one’s speed

of light computers next to the exchanges, which work off a strategy of starting

and ending each day owning nothing, meanwhile leaving today’s counts and

countesses still believing they live in a financial world lead by long term

investors. Only when the busts phase sets in with earnest, will they begin to

wake up to learn that 2% of the 20,000 or so trading firms that made up 73% of

all U.S. equity trading volume have left them holding the bag. (8) (9)

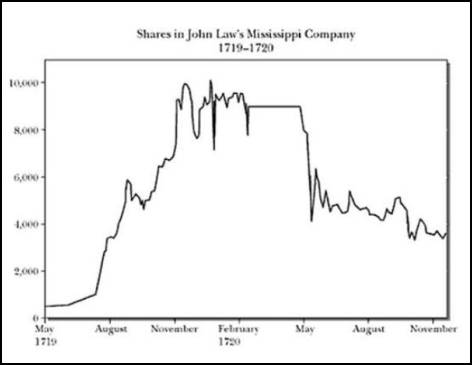

But

let’s return to the 1700s. By the fall of 1719, the shares in the Mississippi

Company were growing in value like a gambler on a roll. The people of France

were enjoying a life of luxury very different from where they had been a mere 4

years earlier. Shares hitting 2,830 livres in August were 4,800 by late

September, then skyrocketed to 6,463 in late October, and 8,975 in late

November. (10)

By

1720, a single share had reached 10,100 livres. What could go wrong!

At

the height of societal excitement to “get in”, a wealthy aristocrat, Prince de

Conti, wanted to cash out his shares. Law did not permit the sale. De Conti then

rounded up all his Banque Royale notes and demanded that his notes be turned

into coins. It wasn’t long before the public was trying to break down the doors

of Banque Royale, and went from their love affair with shares of the

Mississippi Company and their newfound wealth, to a desire for hoarding gold

coins. (11) The collapse of the Mississippi Company’s value and bank

run on the Banque Royale ruined thousands of middle-class French citizens.

Needless

to say, Law was never again seen in a positive light by the people of France

who had been caught up in his experiment of “unlimited riches” with the backing

of the state. Thank goodness we are much too smart for such a thing like this

to happen today.

Early Years of American Finance and The Continental

When

Americans speak of the founding of the nation, they do not speak of the early

days of the nation’s finances. Most likely, it is because they have probably

never been taught about the following piece of history.

The

total value of the money supply of the United States at the start of the

Revolution was $12 million. In order to finance the Revolution, the Continental

Congress launched America’s first paper currency for $2 million and before it

was printed concluded that another $1 million was needed. Before the end of

year (1775) the amount of paper money printed had reached $6 million,

increasing the nation’s money supply $6 million in less than a year. (12)

The

next few years saw a dramatic increase of the “Continental” paper money.

Congress

issued $6 million in 1775, $19 million in 1776, $13 million in 1777, $64

million in 1778, and $125 million in 1779. In 5 years, the nations money supply

had grown from $12 million to $225 million.

This

behavior lead to rapid inflation and the devaluation of the paper money in

terms of specie (coins). In 1776, the

Continentals were worth $1 for every $1.25 of specie. The new money continued

falling in value, hitting a 6.8:1 ratio in 1778, and 42:1 by December 1779. By

early 1781, less than 18 months later, one needed 168 paper Continentals to

exchange for one dollar in specie. (13)

With

these experiences in the minds of the first generation of Americans, we can see

that their experience lead to action by our nation’s leaders. The following was

stated in the December 16, 1789 edition of the Pennsylvania Gazette:

“Since the federal constitution has removed all danger of our having a paper tender, our trade is advanced fifty per cent.”

Historian

Louis Hacker described the period as one “of unexampled business expansion, one

of the greatest, in fact, the United States has had…The exports of the country

mounted from $19 million in 1791 to $93 million in 1801.” In 1792 the federal

deficit was 28 percent of expenditures. By 1802, the deficit had disappeared altogether,

and had been replaced with a surplus equal to the government’s total spending. (14)

Can you even imagine such a thing in an age where political leaders see

going from overspending a trillion in a year to overspending $600 billion in a

year as progress!

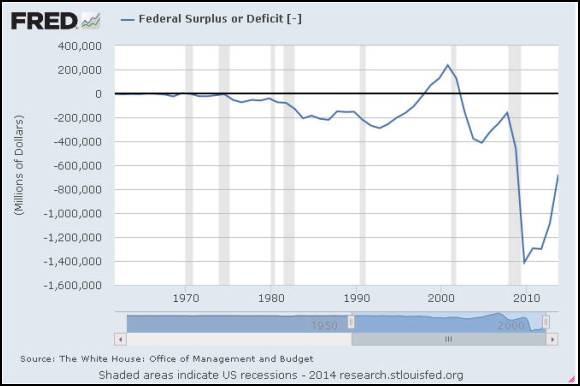

[Source

– Federal Reserve Bank of St Louis]

Look

at the chart above. This research was done by one of the 12 banks that comprise

the Federal Reserve System. Since the 1970s, one can see that the United States

government has spent more than it has brought in, other than a few brief years

in the late ‘90s. September will mark 6

years since hearing of the need for a $700 billion bailout to save the

financial system. Trillions in additional bailouts and stimulus programs have

taken place since 2008. As just stated, our political leaders seem pleased that

our deficit has been reduced to around $600 billion. When will we come to a

point as a society, where we will openly discuss how the power to print

“unlimited” money might fail…again?

Does

anyone in leadership in the financial sector, whether private or public,

remember this saying?

“If

your outgo exceeds your income then your upkeep will be your downfall.”

Where

Is the Scheme Today?

The

scheme today started in 1971, when the dollar was removed from the gold

exchange standard. To make sure we understand how significant this event was in

the history of finance, let’s look back at a few things that took place before

we arrived at 1971.

Through the rise and fall of ancient empires, coins were used. The quality of the coin could be reduced in

value by adding more dross or a lower grade metal as a way to stretch the

empires money. However, paper money and central banks were yet to come. After

the Roman Empire fell, it would take until the1600s before history would see

the first central bank. As already mentioned in this article, this was the

Amsterdam Wisselbank founded in 1609. The first English national debt of long

maturity was floated in 1692 to finance a war with France, and subscribers to

this loan were given the right by the English government to incorporate

themselves as the Bank of England in 1694. (15) The first paper money sanctioned by a government was France

in the early 1700s, which as we have seen, lead eventually to the collapse of

the Mississippi Company’s stock, and a run on the Banque Royale by the people

of France.

Through the rise and fall of ancient empires, coins were used. The quality of the coin could be reduced in

value by adding more dross or a lower grade metal as a way to stretch the

empires money. However, paper money and central banks were yet to come. After

the Roman Empire fell, it would take until the1600s before history would see

the first central bank. As already mentioned in this article, this was the

Amsterdam Wisselbank founded in 1609. The first English national debt of long

maturity was floated in 1692 to finance a war with France, and subscribers to

this loan were given the right by the English government to incorporate

themselves as the Bank of England in 1694. (15) The first paper money sanctioned by a government was France

in the early 1700s, which as we have seen, lead eventually to the collapse of

the Mississippi Company’s stock, and a run on the Banque Royale by the people

of France.

Now let’s leap to the 20th century. On September 20, 1931,

the Bank of England would no longer fill the request to exchange their gold for

any nation demanding payment in gold rather than it paper money, the pound

sterling. This was another first in history. The economist Moritz J. Bonn at

the time wrote, “ [It] was the end of an age. It was the last day of the age of

economic liberalism in which Great Britain had been the leader of the world.

Now the whole edifice has crashed. The slogan ‘safe as the Bank of England’ no

longer had any meaning.” (16)

Now let’s leap to the 20th century. On September 20, 1931,

the Bank of England would no longer fill the request to exchange their gold for

any nation demanding payment in gold rather than it paper money, the pound

sterling. This was another first in history. The economist Moritz J. Bonn at

the time wrote, “ [It] was the end of an age. It was the last day of the age of

economic liberalism in which Great Britain had been the leader of the world.

Now the whole edifice has crashed. The slogan ‘safe as the Bank of England’ no

longer had any meaning.” (16)

As

the most documented war of all time was coming to an end, World War II, world

financial leaders were working on a plan to kick-start the global economy.

Economists Dexter White (American) and John Maynard Keynes (British) were the

two individuals brought in to draft a solution. Both would espouse substantial

inflation (the massive increase of money, i.e. debt) as the basis of rebuilding

the world economy. Keynes envisioned a new international monetary unit called

the bancor. World financial leaders did not embrace this idea at the time, and

in the end, it was the US dollar fixed at a value of $35 per gold ounce that

would become the basis for this new global monetary order. (17) (18)

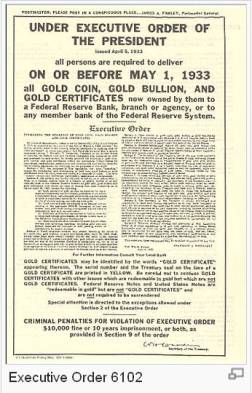

The US government had already made it illegal for Americans to hold

gold as a form of money in 1933 - something that had been a form of money back

through ancient empires. Instead, central bankers would now place American

dollars in their banks, since these dollars could be exchanged for gold if

demanded. In other words, the dollar was as “good as gold” (19)

Everyone had already seen what could happened when too much money was printed

up for the gold that was suppose to back it, as the Bank of England had shown

in 1931. So it was no surprise to those who had studied financial history when

it happened again in August 1971 with the American dollar.

The US government had already made it illegal for Americans to hold

gold as a form of money in 1933 - something that had been a form of money back

through ancient empires. Instead, central bankers would now place American

dollars in their banks, since these dollars could be exchanged for gold if

demanded. In other words, the dollar was as “good as gold” (19)

Everyone had already seen what could happened when too much money was printed

up for the gold that was suppose to back it, as the Bank of England had shown

in 1931. So it was no surprise to those who had studied financial history when

it happened again in August 1971 with the American dollar.

So

on August 15, 1971, right before I entered my freshman year of high school,

President Nixon announced to the American people and world, “We must protect the

American dollar as a pillar of stability around the world”. What was the

solution to protecting the US dollar as a “pillar of stability”? The same

solution delivered to global financial markets and banks in 1931. The US government

would no longer honor its promise to exchange dollars for gold by those nations

losing faith in our own government’s increasing debt load, or concerned about

the stability of the American dollar. On its 40th anniversary in

2011, the dollar had declined to a point where it was only worth 19 cents of

its 1971 value. (20)

“Infinity and Beyond” is a Lie

Sadly,

living through the last 40 years of history where no major industrial nation

has backed their currency by gold, the devaluation of currencies has been in a

race to the bottom. We all need currency (whether electronic or paper) to live

out our own individual lives day to day. The world that brings so many things

to our homes and businesses is an extremely complex interdependent global system. Adding more and more debt only increases

risks across the entire system.

Yet,

after 1971, every financial crisis had to be explained as anything other than

the devaluation of the currency, and inflation was anything but the printing of

money and increasing of our national debts. If this was explained clearly to

the public, it would be obvious that the only bank given the power to print the

American dollar, the Federal Reserve, was at the root of our of nation’s

growing financial problems. The same applies to the printing presses of central

bankers worldwide, and the nations they serve.

We

are all watching a tragicomedy unfold, that will eventually bring far more

tragedy than comedy.

The

results are always the same once the public has come over the next financial

mountain in history; destruction of wealth and changes that impact everyone,

whether rich or poor.

These

changes will come. History has shown that repeatedly. Promoting the idea that

“investors” are excited about the latest central banking scheme to continue

markets at “all time high” levels has a limited shelf life. This is only

feeding the public a lie, that today’s global Mississippi Scheme is on track to

bring even greater riches to those who put their fear behind them, forget everything

in history that brought us to this point, and place their trust in the idea

that never ever will central bankers let a problem show up in financial markets

again that can not be solved by more debt, more central planning, and more

direct intervention.

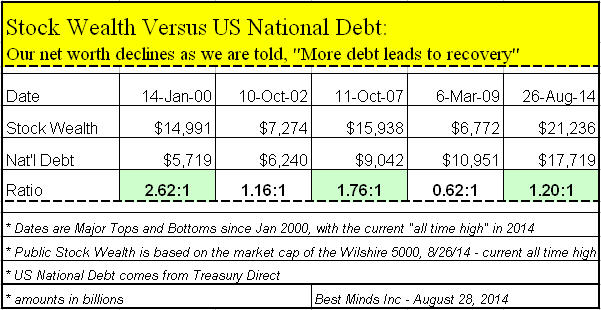

Equities

Reach Record $66 trillion as S&P 500 Hits 2,000, Bloomberg, Aug 27

“Rallies

from Brazil to Japan and the Standard & Poor’s 500 Index’s first trip above

2,000 sent the value of global equities to a record $66 trillion….

‘Geopolitical

events are significant and major new attacks are tragic, but they’re not enough

to unsettle the global economic forces in play, especially in America,’ said

Patrick Spencer, head of U.S. equity sales at Robert W. Baird & Co. in

London. ‘Draghi gave clear indication that he’s standing ready with further

measures to stimulate growth and that’s helping overall sentiment.’…

The

value of equities globally has soared from $25 trillion in March 2009. Stocks

were valued at $63 trillion at the 2007 peak, according to data compiled by

Bloomberg.”

IMF

paper warns of 'savings tax' and mass write-offs as West's debt hits 200-year

high, UK Telegraph, Jan 2 ‘14

“Much of the Western

world will require defaults, a savings tax and higher inflation to clear the

way for recovery

as debt levels reach a 200-year high, according to a new report by the

International Monetary Fund.

The IMF working paper

said debt burdens in developed nations have become extreme by any historical

measure and will require a wave of haircuts, either negotiated 1930s-style

write-offs or the standard mix of measures used by the IMF in its “toolkit” for

emerging

market blow-ups.”

Escaping

from reality is enjoyable when decisions and life are hard, and you need a

brief rest. Living outside reality only means being awakened back into a world

that is much harsher when thrust upon us.

When Booms End, Busts Begin

If

you are not spending hours connecting the dots of these powerful world trends,

and seeking to understand how to make changes for the financial landscape

ahead, I would strongly suggest the paid research newsletters and

trading reports available with a six month subscription

to The Investor’s Mind. Money is

always moving. Bulls become bears and bears become bulls.

The

cost of good research and critical thinking has become extremely small

considering the money that can evaporate during the downside of financial

schemes.

*

Contact my office if you have an interest in public speaking, media interview,

or consulting.

*

Riders on the Storm: Short Selling in Contrary Winds (Jan ’06) was a

research paper I wrote on how investors are deceived, and contains interviews

with industry famous contrarians. It can be downloaded

for free.

Sources:

(1)

My Oct 31, 2013 article, Who

Needs God, We Have Bankers, and David Stockman’s June 6, 2014 article, Draghi’s

Horrible Threat: “Are We Finished Yet? The Answer Is No!”

(2) Devil

Take the Hindmost: A History of Financial Speculation (1999), Edward

Chancellor, pg 9, used in The Investor’s Mind, Feb 2007, A New World Order:

Explorers, Speculators, and Debt Managers

(3) Financial

Reckoning Day: Surviving the Soft Depression of the 21st Century

(2003), William Bonner with Addison Wiggins, pg 72

(4) Ibid, pg

78

(5) Picture located

at Mississippi History Now, John Law and the Mississippi Bubble:1718-1720, http://mshistory.k12.ms.us/articles/70/john-law-and-the-mississippi-bubble-1718-1720

(6) Financial

Reckoning Day, Bonner, pg 81

(7) Extraordinary

Popular Delusions & the Madness of Crowds, Forward by Andrew Tobias (1980,

originally published in 1841) Charles Mackay, pg 15

(8) Broken

Markets: How High Frequency Trading and Predatory Practices on Wall Street Are

Destroying Investor’s Confidence (May 2012), Sal Arnuk and Joseph Saluzzi, location

484 of 5286 in Kindle Edition

(9) Treasury’s War: The Unleashing of a New Era

of Financial Warfare (Sept 2013) Juan Zarate, location 6441 of 9698 in Kindle

Edition

(10)

Financial Reckoning Day, Bonner, pg 81

(11)

Ibid, pg 84

(12) History of Money and Banking in the United States: The Colonial Era to World

War II (2002), Murray Rothbard, edited by Joseph Salerno, pg 59

(13)

Ibid, pg 59-60

(14) The Creature from Jekyll Island: A Second Look at the

Federal Reserve, Third

Edition (1998), G. Edward Griffin, pg 322

(15) A History of Interest Rates, Third Edition (1996)

Sidney Homer and Richard

Sylla, pg 126

(16)

History of Money and Banking in the United States, Rothbard, pg 431

(17)

Ibid, pg 480-483

(18) The

bancor has been in discussion since 2008 by world bankers. On the

Research page of the Best

Minds Inc website, I posted an IMF white paper,

Reserve Accumulation and International

Monetary Stability (April 13 ’10) on

March 23, 2011. The following is stated in this IMF

white paper: “From SDR to

bancor – Limitation of the SDR (Special Drawing

Rights) as discussed

previously is that it is not a currency.… A

more ambitious reform option would

be to build on the previous ideas and develop, over

time, a global currency.

Called for example, bancor, in honor of Keynes,

such a currency could be used

as a medium

of exchange…”

(19)

Chart at Executive Order 6102, Wikipedia, http://en.wikipedia.org/wiki/Executive_Order_6102

(20) Forty

Years Ago Today Nixon Took Us Off the Gold Standard, Fox News,

August 15, 2011

Doug Wakefield

President

Best Minds Inc. a Registered Investment

Advisor

1104

Indian Ridge

Denton,

Texas 76205

Phone

- (940) 591 - 3000

Best Minds, Inc is a registered investment advisor that looks to the best minds in the world of finance and economics to seek a direction for our clients. To be a true advocate to our clients, we have found it necessary to go well beyond the norms in financial planning today. We are avid readers. In our study of the markets, we research general history, financial and economic history, fundamental and technical analysis, and mass and individual psychology.